Rendezvous Robotics is raising a $15M Seed round at a $50M post-money valuation, co-led by Toyota Ventures, the University of Michigan Endowment, and MaC Venture Capital, with participation from BlackRock, In-Q-Tel, and Astera Institute, among others. The round follows a $5M Pre-Seed and funds a critical execution window as the company transitions from technical validation to on-orbit deployment and customer-funded programs. Demand has heavily oversubscribed the priced round, and the company is accepting up to $3M in additional capital via a SAFE at a $65M cap to accommodate the overage. We’re actively working with the company to secure allocation in the priced round.

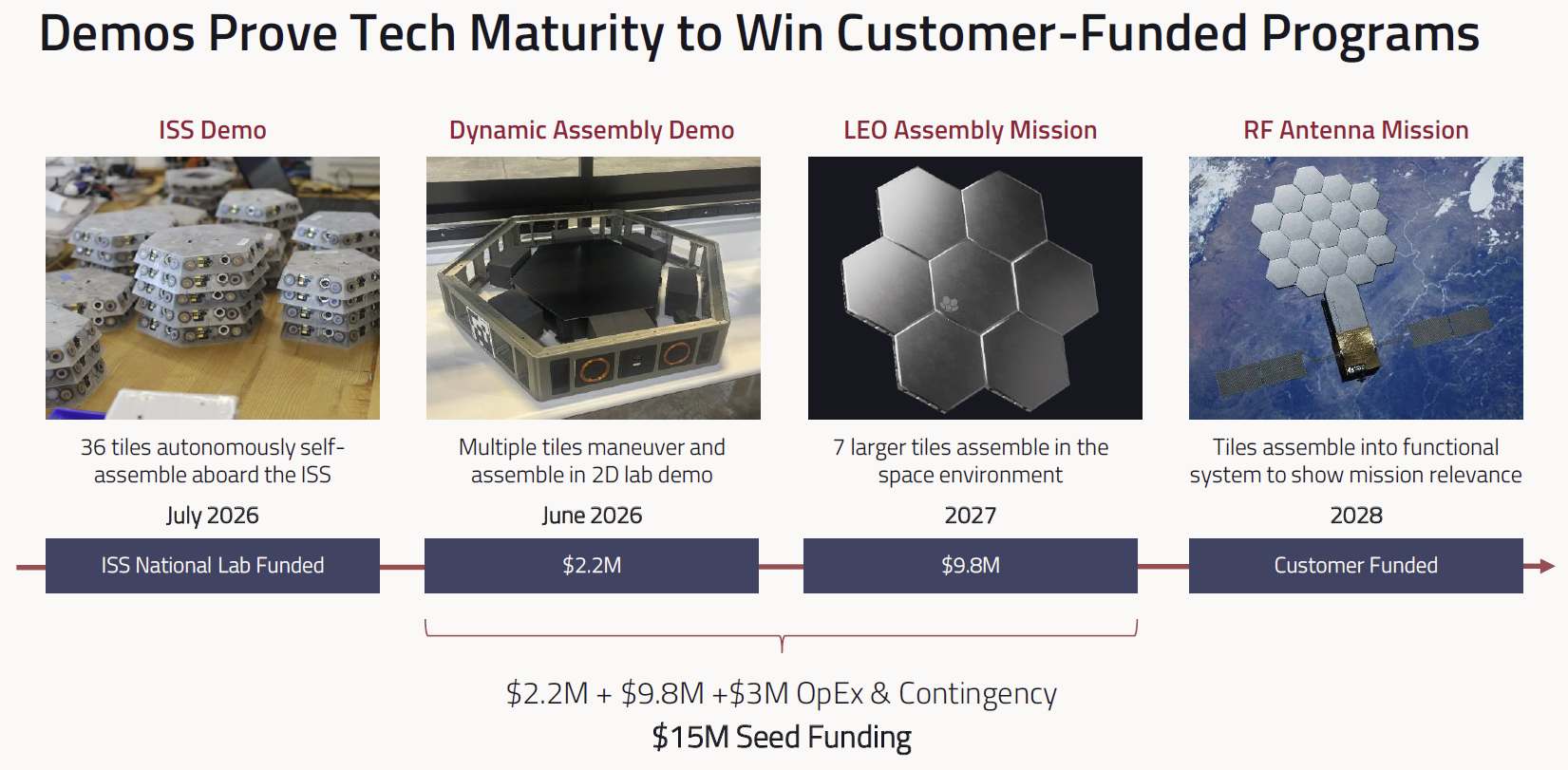

Three near-term milestones anchor the path forward: a ground-based dynamic assembly demonstration in June, a 36-tile autonomous self-assembly mission aboard the ISS in July funded by the International Space Station (ISS) National Lab, and a seven-tile low Earth orbit (LEO) assembly mission in 2027. Together, these demonstrations validate autonomous in-space assembly at scale, de-risk the technology for government and commercial customers, and unlock a pipeline of downstream contracts.

Early customer demand is already taking shape. The company has secured Memorandum of Understandings (MOUs) across defense and commercial customers, including Astranis, HawkEye 360, and Starcloud, alongside a strategic collaboration with Lockheed Martin and active engagement with U.S. government stakeholders. These programs span high-value use cases including Intelligence, Surveillance, and Reconnaissance (ISR), secure communications, and orbital compute, and represent a credible path from demo to funded deployment over the next 24-36 months.

With over eight years of R&D, flight-tested prototypes, and a 2026 ISS mission already in motion, Rendezvous enters this round with rare technical maturity for a company at this stage. The combination of validated technology, early customer pull, and alignment with both defense budgets and commercial space demand positions the company to establish the standard modular platform for next-generation space infrastructure. And it sets up a Series A anticipated in late 2027.

INVESTMENT TIMELINE

In-Person & Virtual Company Presentation

Thursday, June 18th, 2026

5:00 pm ET // 2:00 pm PT

RSVP to the in-person event by emailing Mark Njama (mark@plumalley.co)

Register for the live stream here

Recordings of the Presentation

Part A: Fireside Chat with Ariel Ekblaw, PhD (Co-Founder & Inventor) — An engaging conversation on the future of building at scale beyond Earth and the technologies enabling the next generation of space infrastructure. Access the recording here.

Part B: Founder Presentation with Phil Frank (Co-Founder & CEO) — Hear directly from the Rendezvous Robotics team on their vision, technology, and path toward large-scale construction in orbit. Access the recording here.

Final Investment Commitments Due

Thursday, July 16th, 2026

We will take commitments on a rolling basis. To secure your allocation, please submit final commitments here.

Funding & Documents Due

Thursday, July 23rd, 2026

At the end of the commitment period, you will receive details regarding closing documentation and wiring instructions via Carta.

The Company's confidential financing documents and diligence materials are available for review in Carta. Please request access to data room materials at the top of the page. All documents are confidential and not for further distribution. Plum Alley Ventures Company reserves the right to not proceed with the investment opportunity if the $500,000 syndication minimum is not met.

To learn more, watch the TED Talk below from Co-Founder & Investor Ariel Ekblaw, PhD on building scalable infrastructure in space.

Rendezvous Robotics was founded in 2024 to solve one of the most consequential engineering challenges in the emerging space economy: how to build large, reliable structures in orbit. Headquartered in Golden, Colorado, the company is commercializing TESSERAE — a modular, self-assembling spacecraft architecture invented at the MIT Media Lab by Dr. Ariel Ekblaw.

TESSERAE is built from hexagonal tiles that launch flat-packed in any rocket fairing and autonomously assemble in orbit using electromagnetic actuation and edge-based sensing. Each tile integrates compute, power, thermal, and payload capabilities into a single unit, forming a distributed spacecraft that scales linearly in both size and performance.

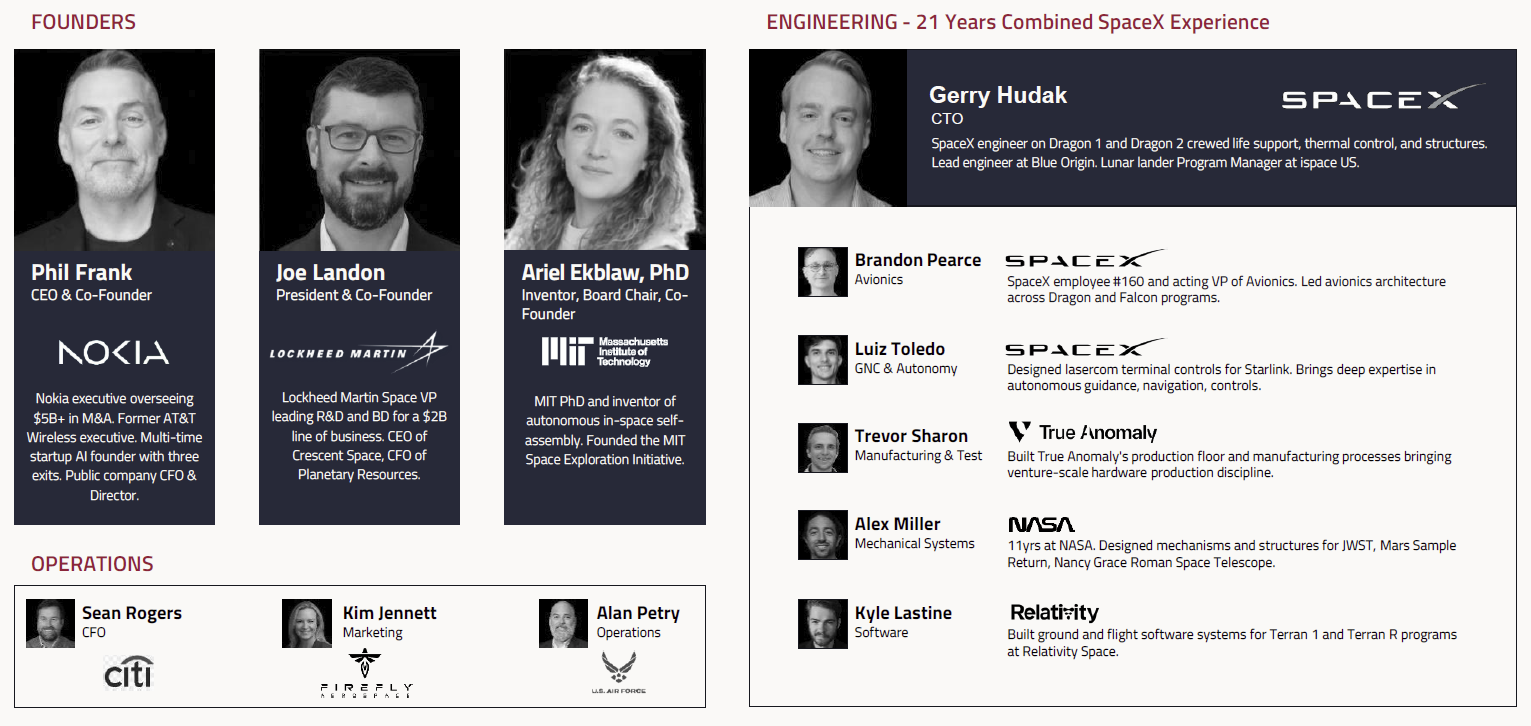

The founding team brings together deep technical invention and hard-won operational experience. Ariel Ekblaw (Co-Founder & Inventor) holds a PhD from MIT and founded both the MIT Space Exploration Initiative and the Aurelia Institute. Phil Frank (Co-Founder & CEO) is a former Nokia M&A executive with multiple startup exits. And Joe Landon (Co-Founder & President) previously served as VP of Advanced Programs at Lockheed Martin Space, CEO of Crescent Space, and CFO of Planetary Resources.

Since coming out of stealth, the company has moved quickly. The Pre-Seed round built the engineering team to 10.5 FTEs, stood up the Golden production facility, delivered hardware for the July 2026 ISS mission, secured the MIT license for the foundational patent, and completed preliminary design review (PDR) for the LEO assembly demonstration.

The company has moved beyond core Research and Development (R&D) into early system deployment, signaling a clear transition toward commercialization. Over eight years of development, Rendezvous has advanced through multiple generations of hardware, validating magnetic self-assembly in microgravity, demonstrating autonomous assembly aboard the ISS, and completing multi-tile 3D assemblies in flight-like environments. The current Gen-5 system represents production-ready hardware, with 36 tiles already delivered for a July 2026 ISS mission that will autonomously assemble in orbit and validate system performance at scale.

In parallel, Rendezvous has built meaningful pull across defense and commercial markets. The company has signed MOUs with Astranis, HawkEye 360, Starcloud, and Broadcom, alongside strategic collaboration with Lockheed Martin on space protection systems and engagement with US government stakeholders shaping next-generation programs. Letters of Support from Lockheed Martin, L3Harris, NASA Goddard, AFRL, and Blue Canyon Technologies, combined with active NDAs across a range of primes and operators, reinforce early demand across communications, ISR, orbital compute, and space protection.

Together, this positions Rendezvous as more than a spacecraft manufacturer. The company is establishing a modular standard for how systems are built in orbit, where each deployment expands the tile catalog, compounds capability, and strengthens its role as the underlying platform for next-generation space infrastructure.

The in-space assembly market is driven by three forces that are converging at once.

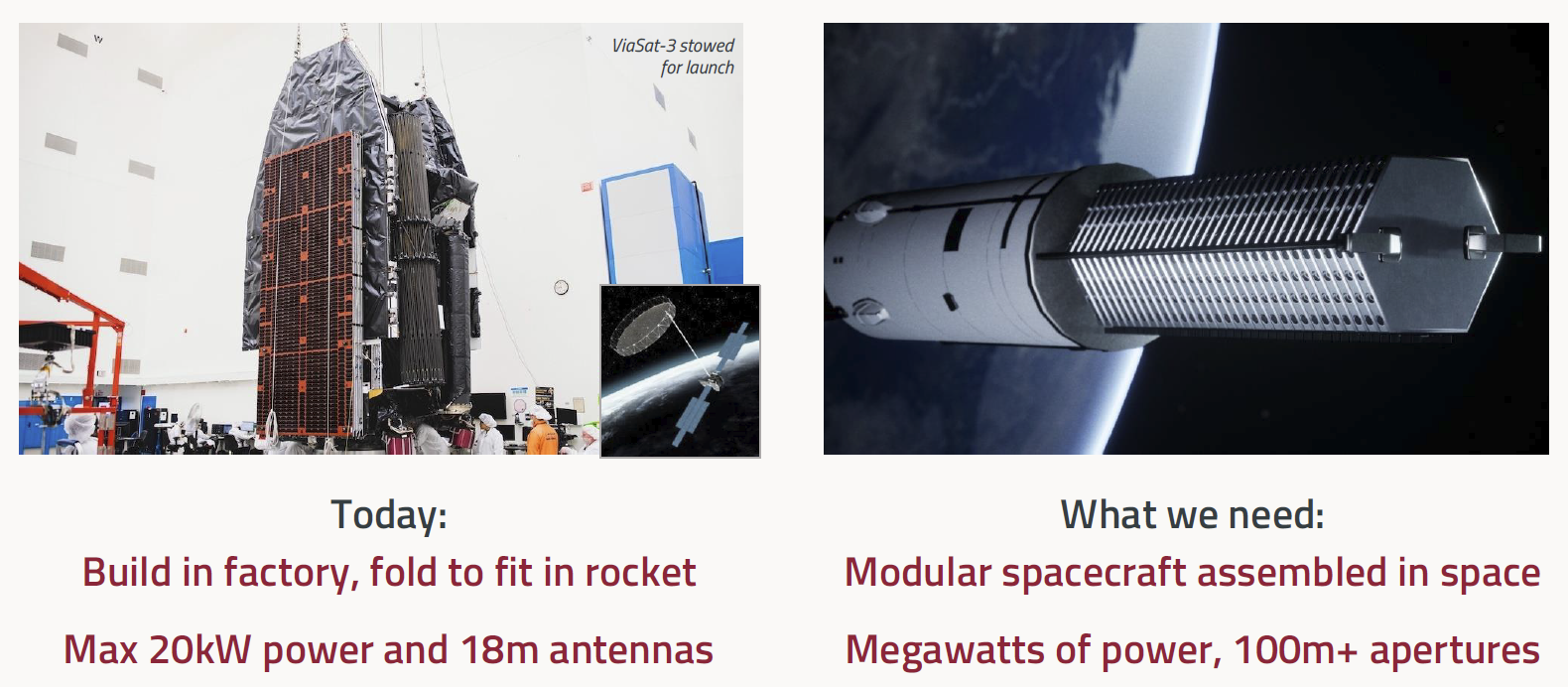

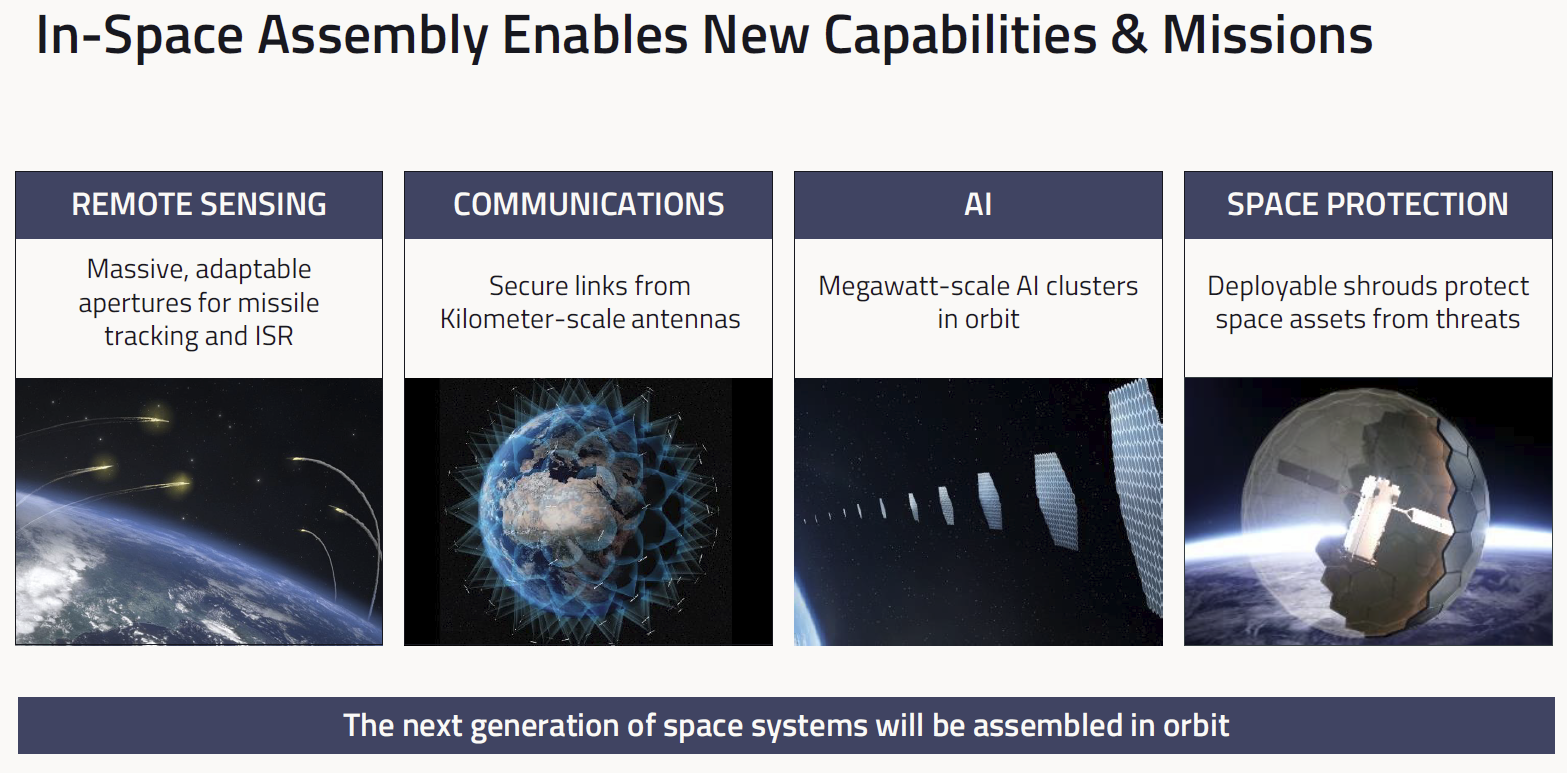

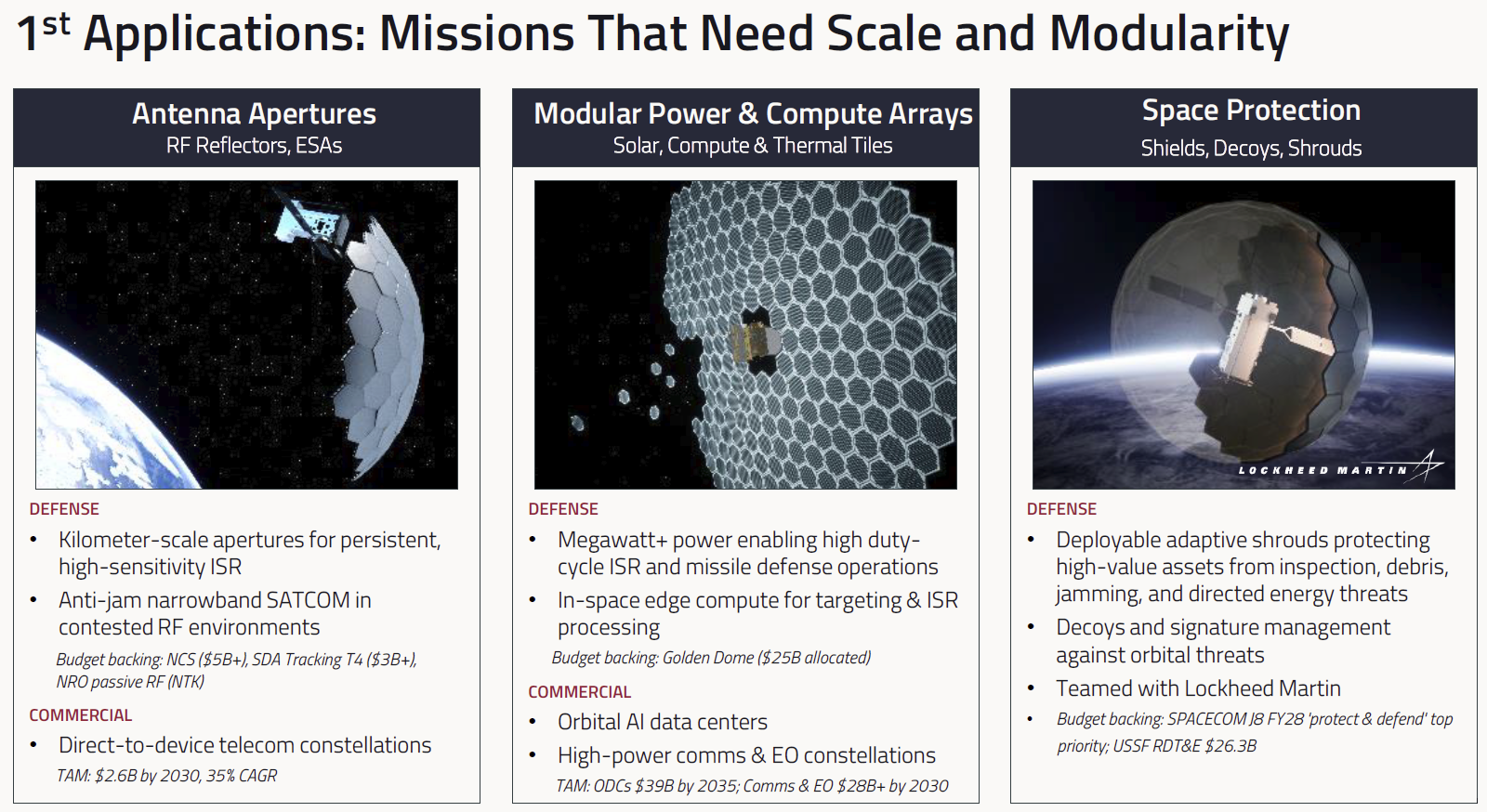

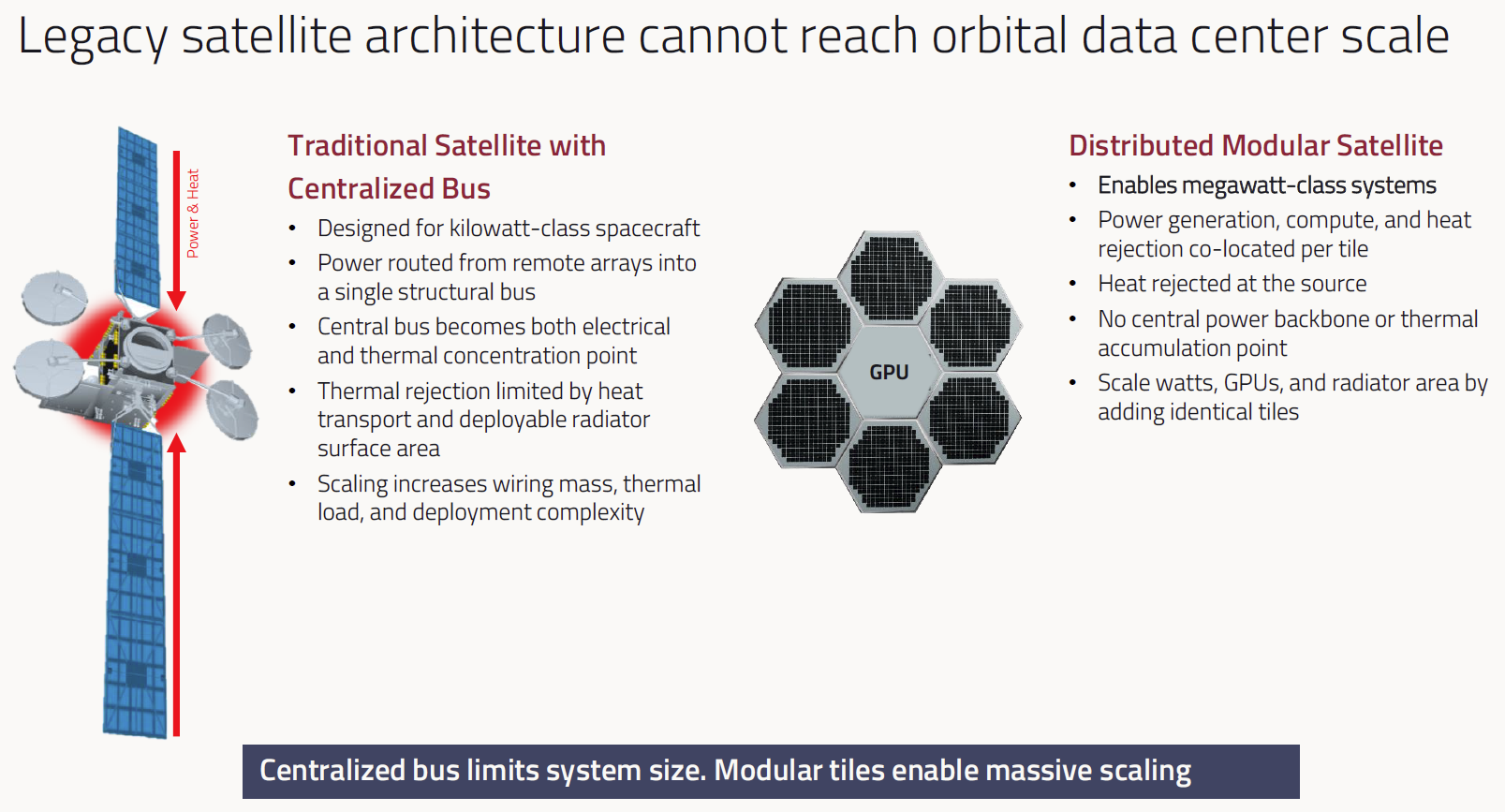

1: A physical ceiling. Every spacecraft has been folded to fit inside a rocket fairing. That design paradigm has hit its limits. Even ViaSat-3, one of the most advanced commercial satellites ever built, tops out at ~20 kilowatts of power and an 18-meter antenna after decades of iteration. The next wave of missions, including orbital AI compute clusters, missile defense constellations, kilometer-scale Intelligence, Surveillance, and Reconnaissance (ISR) systems, and anti-jam narrowband SATCOM, demands megawatts of power and 100-meter-plus apertures. Folded architectures cannot scale to meet those requirements. This is not an engineering optimization problem. It is a structural ceiling.

2: Defense modernization. Golden Dome carries $25B for space-based missile tracking and active defense. United States Space Command has named “protect and defend” its top FY28 priority, while United States Space Force RDT&E spending stands at $26.3B annually. Programs like Narrowband Communications Satellite ($5B+), SDA Tracking Layer Tranche 4 ($3B+), and National Reconnaissance Office passive RF initiatives are actively funded. These missions require scale, rapid reconfiguration, and resilience, capabilities that align with autonomous tile assembly and strain legacy deployables. This is not speculative demand. These are funded programs with defined requirements.

3: Commercial demand. Orbital data centers are projected to reach $39B by 2035, driven by abundant solar power and constrained terrestrial siting. Direct-to-device SATCOM is expected to hit $2.6B by 2030 at a 35% CAGR, with players like Globalstar, Viasat, Intelsat, SES, and Lynk Global pursuing next-gen apertures. High-power communications and Earth observation add another $28B+ by 2030. Across all segments, aperture, power, and thermal constraints define system limits. Tile-based assembly removes those constraints at the architectural level.

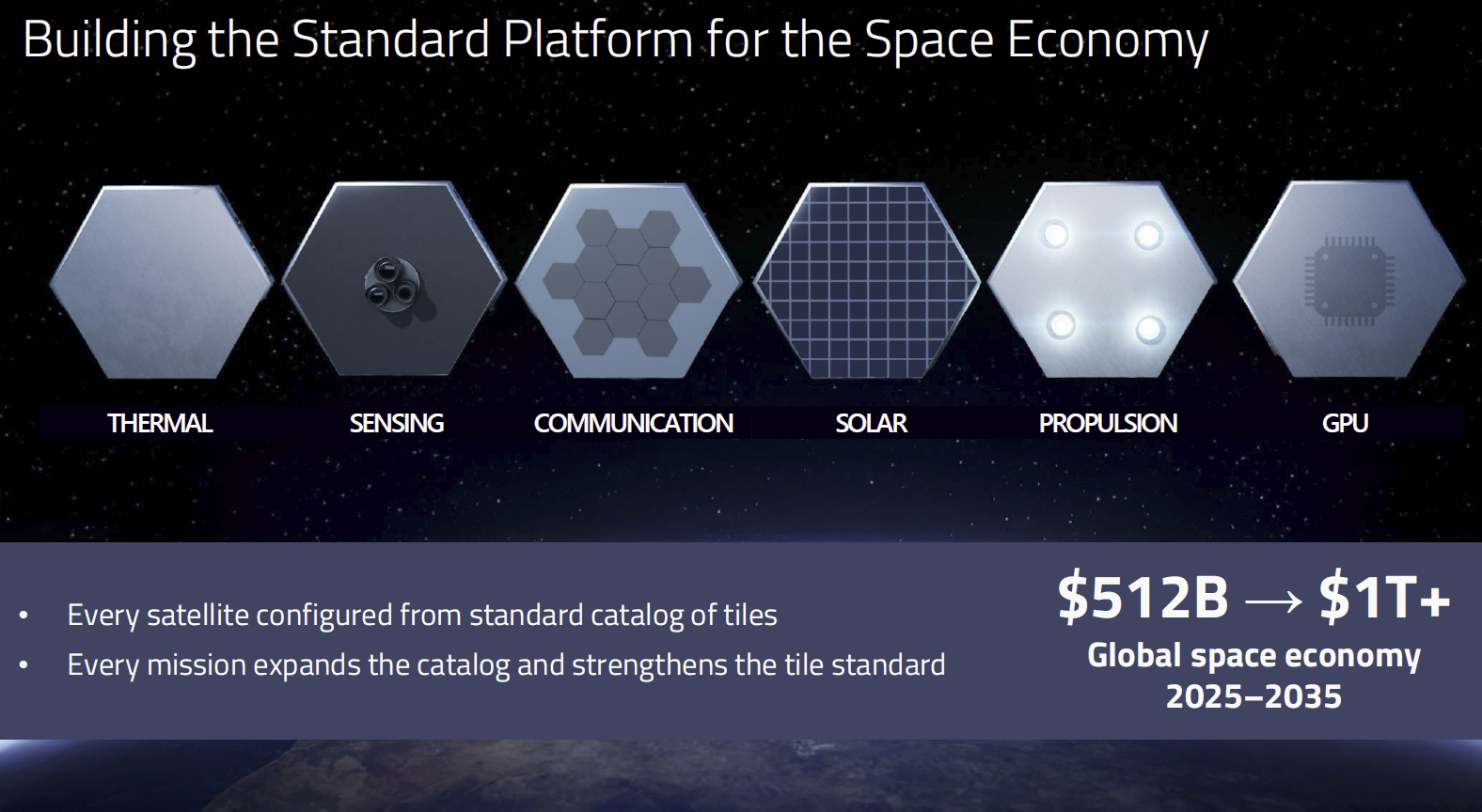

The global space economy stands at ~$512B and is projected to exceed $1T by 2035. The growth that matters sits in missions that cannot be folded into a rocket. That is Rendezvous Robotics’ wedge, concentrated in the highest-value segments where scale drives outcomes. This mirrors the transition from discrete components to integrated circuits. The shift from bespoke deployables to tile-composed spacecraft is a generational reset, and the company that defines the standard early is positioned to own the category for decades

Rendezvous Platform

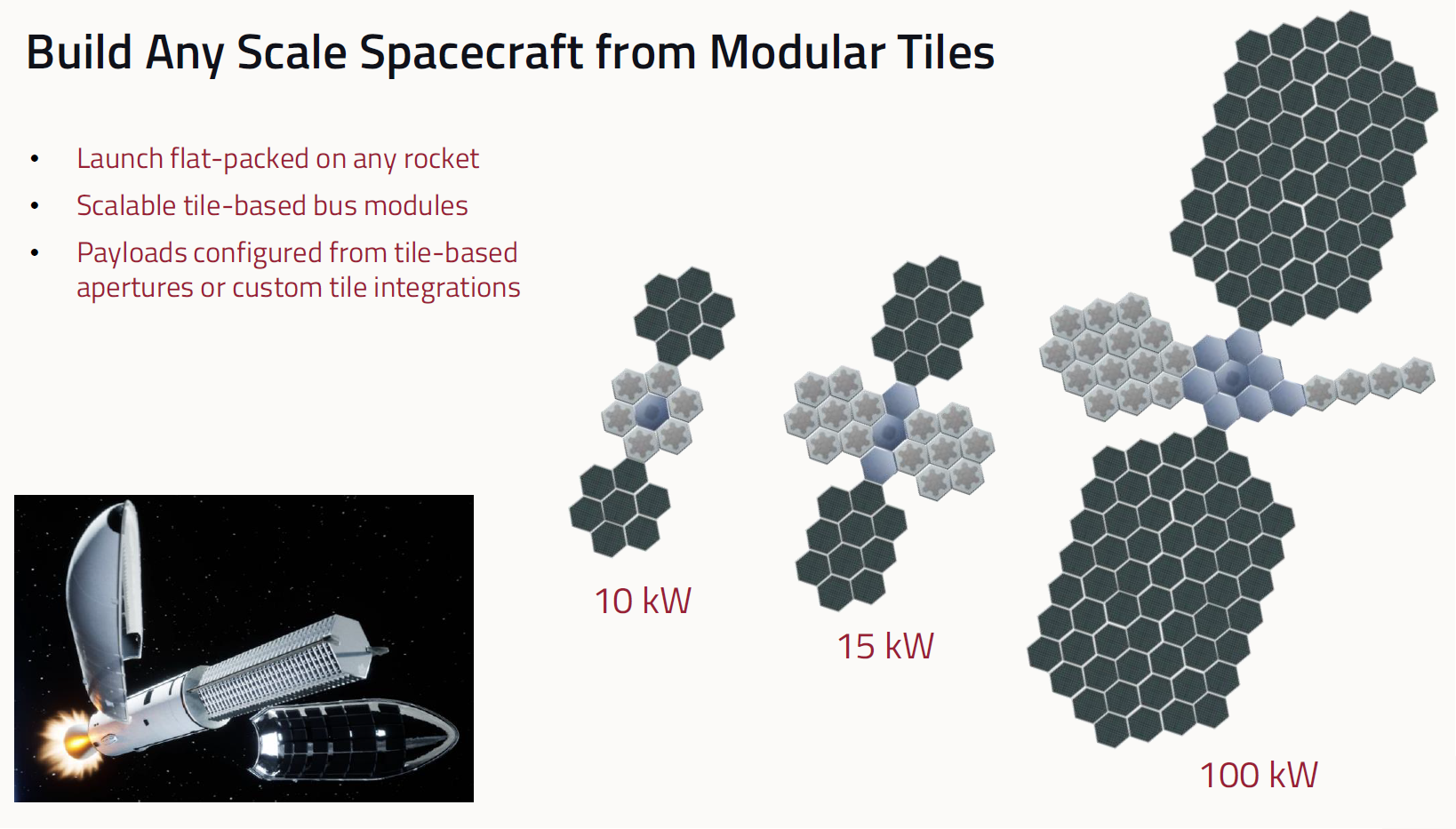

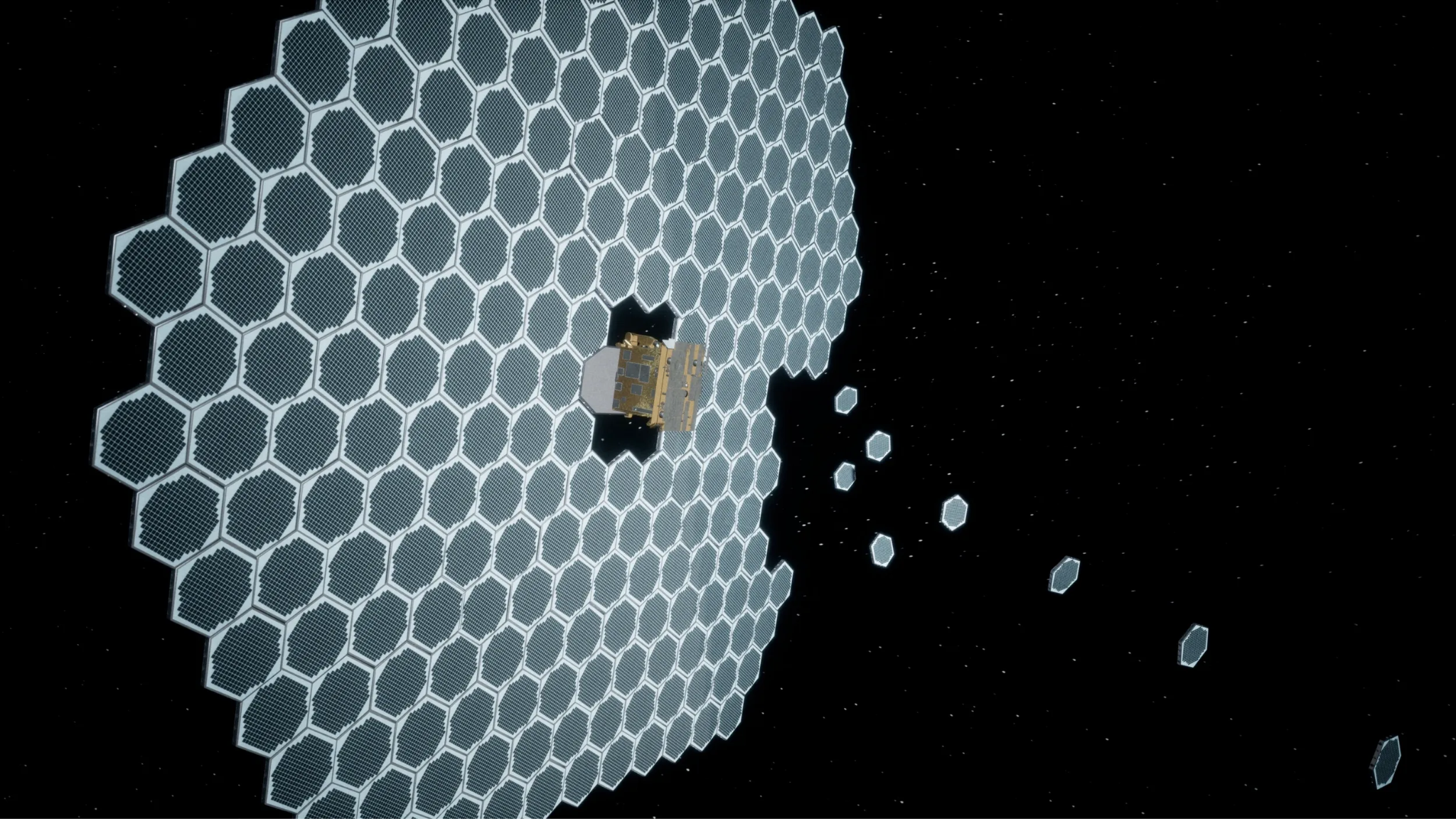

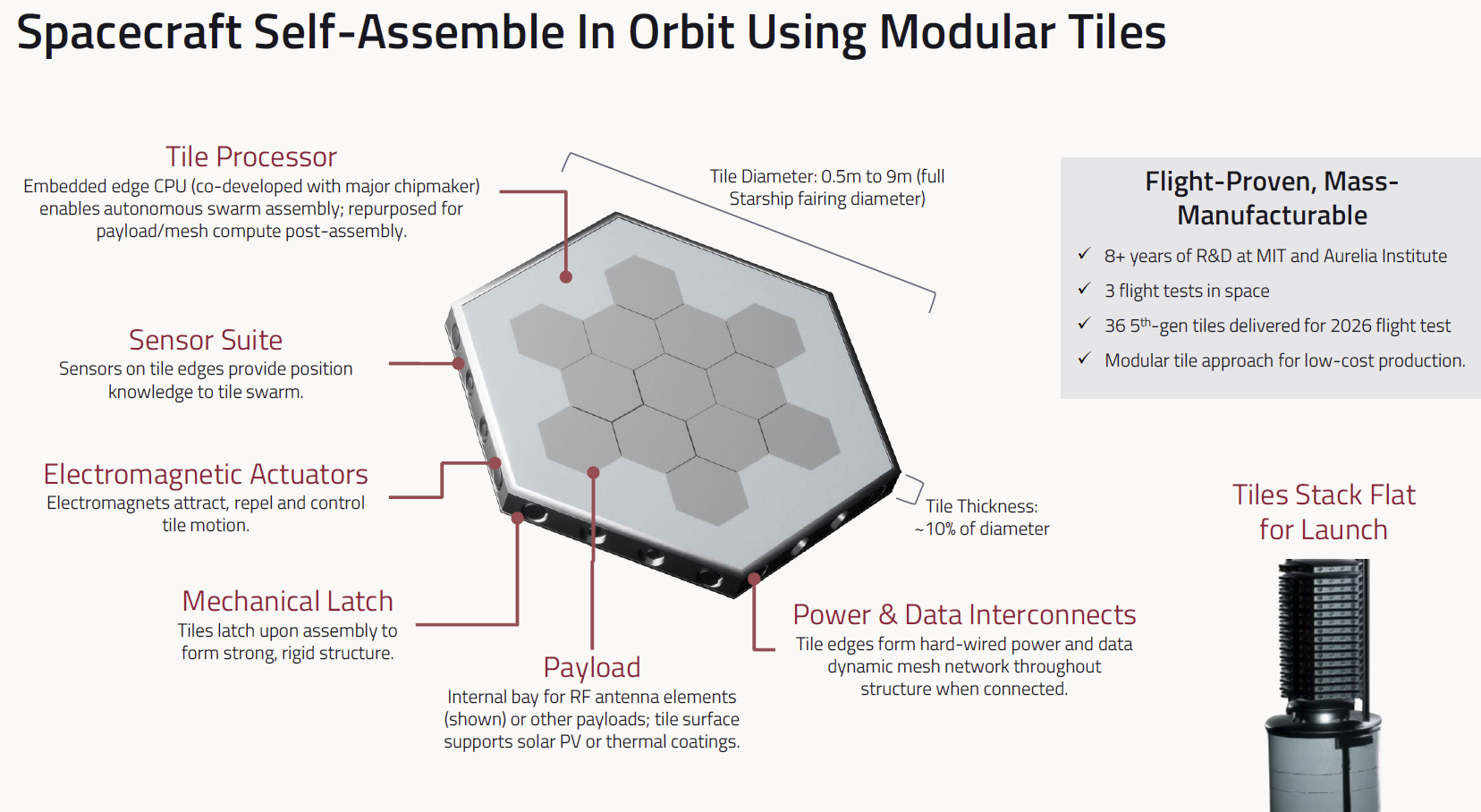

The Rendezvous platform is a vertically integrated autonomous in-space assembly system built around a single modular primitive: the hexagonal tile. Each tile is effectively an autonomous spacecraft in its own right, carrying a Broadcom-co-developed embedded tile processor, electromagnetic actuators for proximity operations and attitude control, an edge sensor suite for swarm position knowledge, mechanical latches that form rigid post-assembly structure, and tile-edge power/data interconnects that create a dynamic mesh across the assembled system. Tiles range from 0.5 meters to 9 meters in diameter (full Starship fairing diameter), with thickness approximately 10% of diameter, enabling dense flat-pack launch configurations on any rocket. The internal payload bay supports modular integrations (radio frequency [RF] antenna elements, solar photovoltaics, thermal coatings, GPU accelerators, sensing payloads) making the same tile bus configurable to dramatically different missions.

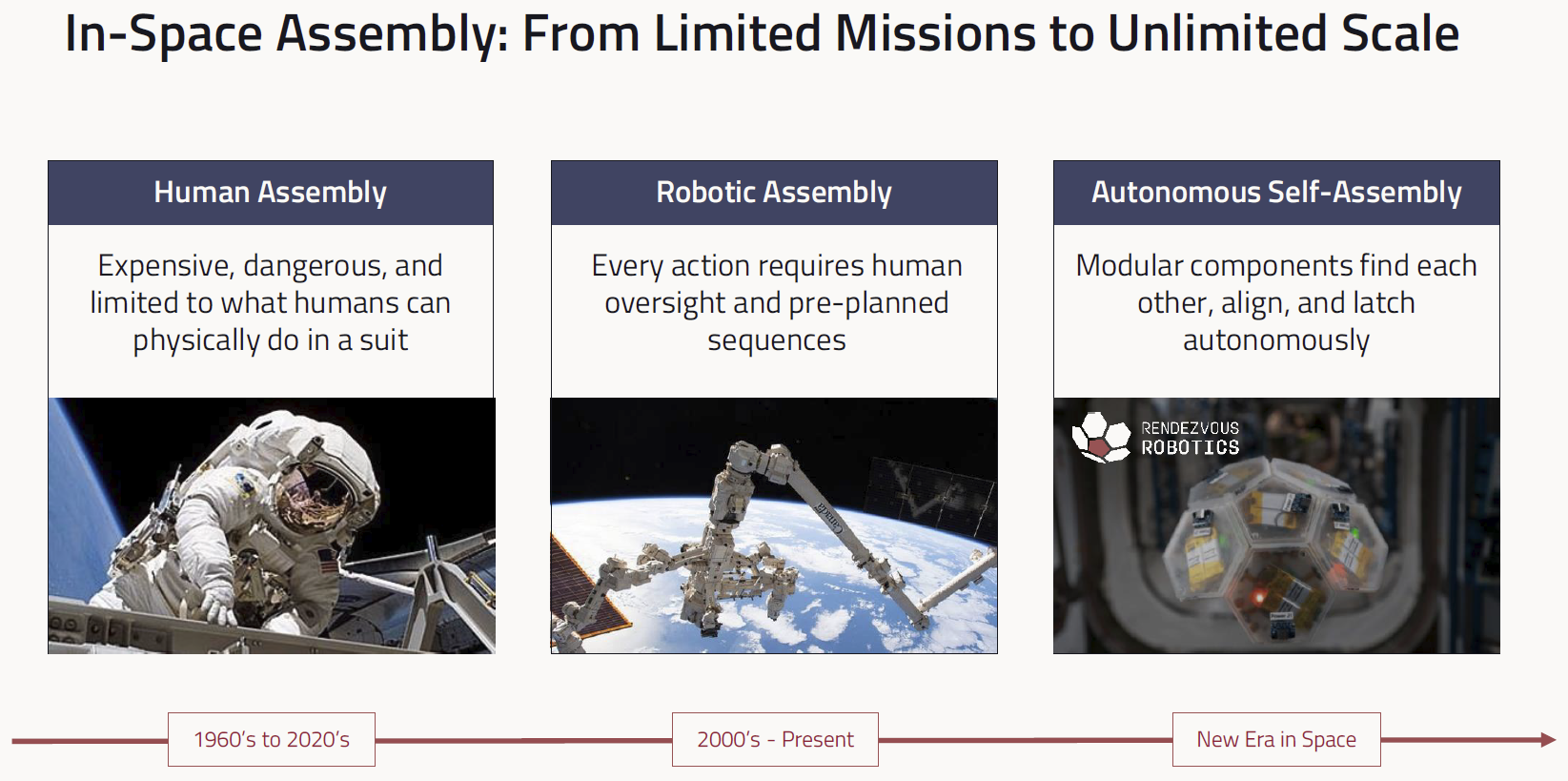

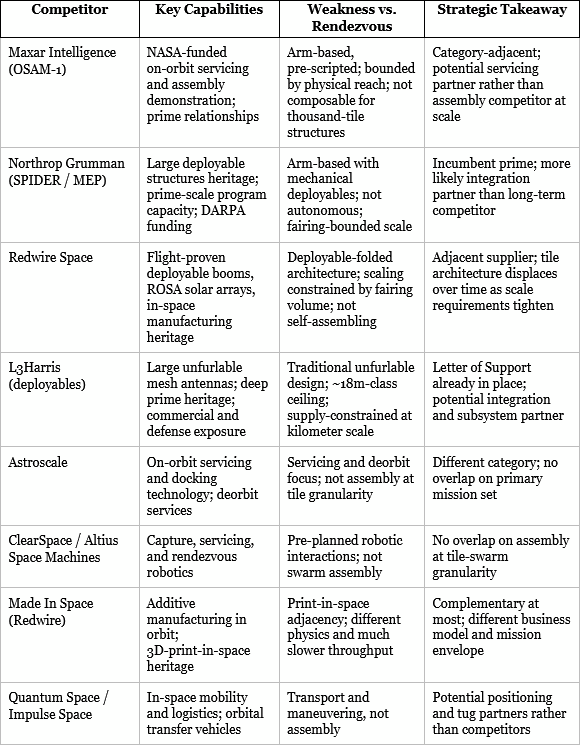

What separates this architecture from prior in-space assembly work is autonomy, not scale alone. Human Extravehicular Activity (EVA) assembly, used to construct the International Space Station over dozens of missions and roughly $100B, is expensive, dangerous, and limited to what a suited astronaut can physically manipulate. Robotic arm assembly — the approach pursued by Maxar's OSAM-1, Northrop Grumman's SPIDER, and adjacent satellite-servicing programs — requires pre-scripted sequences under continuous human oversight and is structurally bounded by the reach of the arm. Autonomous electromagnetic self-assembly is categorically different: tiles find each other, align, and latch without supervision, and the assembled structure can reconfigure, self-correct, or replace degraded modules on orbit. This shift is analogous to the transition from hand-tooled manufacturing to CNC-automated production on Earth, and it unlocks scale that neither predecessor can approach.

Autonomy, Mesh Compute, and Distributed Thermal Management

A second layer of defensibility sits in the post-assembly use of the tiles. Once latched, embedded processors across the assembled structure form a distributed compute mesh, with power generation and heat rejection co-located at each node. This directly addresses the thermodynamic problem that makes centralized orbital compute unbuildable: solar power in orbit is abundant, but without an atmosphere there is no efficient path to reject heat from a dense compute core. Traditional orbital data-center concepts, which copy terrestrial density and wrap a compute core in radiator arrays, fail on this single constraint. Distributing accelerators across the structure (tunable to the mission, whether one in every tile, every fifth, or every tenth) makes thermal density a design parameter rather than a constraint. The same architecture that enables physical scale also enables scalable edge inference, persistent ISR processing, and autonomous on-orbit mission reconfiguration.

The Broadcom custom silicon co-development agreement targets a tiered roadmap aligned to this architecture: lightweight controllers in every tile for autonomy and power management; mid-range processors for cluster coordination and mesh communications; and high-end compute tiles for local AI workloads and inference clusters. As production volumes scale from the hundreds of tiles in early missions to the thousands and eventually millions envisioned for constellation-scale deployments, silicon economics compound tile-level unit economics and establish a durable hardware flywheel between Rendezvous and a category-defining networking silicon partner.

Development Process: From Lab to Orbital Platform

Rendezvous has compressed eight years of MIT-originated research into a disciplined development pipeline organized around successive flight demonstrations. Gen-1 tiles validated basic electromagnet polarity and docking physics on ZeroG parabolic flights in 2017 and 2019. Gen-2 demonstrated the first magnetic self-assembly in microgravity on ZeroG and Blue Origin NS-11 in 2019 and validated electropermanent magnet performance. Gen-3 and Gen-4 achieved subscale autonomous assembly inside the ISS on SpaceX CRS-20 in 2020 and Axiom-1 in 2022, simultaneously validating the hardware and the underlying simulation environment. Each generation added capability while retaining the core primitive (hexagonal, electromagnetically actuated, autonomously commanded) such that lessons compounded rather than reset.

Gen-5, the commercial generation, marks the transition from research to production. The platform completed full 32-tile complex 3D assembly on ZeroG flights in November 2024 and May 2025, and 36 Gen-5 flight units are integrated and manifested for the July 2026 ISS demonstration on JAXA's HTV-X2 — the company's third orbital demonstration overall and its first at full operational complexity. The two subsequent gates are already scheduled: a June 2026 ground-based 2D dynamic assembly demonstration testing multi-tile maneuvering under realistic control conditions, and a Q1 2027 seven-tile LEO assembly mission testing larger tiles in the actual space environment. A 2028 RF antenna mission, targeting tiles assembling into a functional system with demonstrable mission relevance, is planned to be customer-funded — the commercial inflection event.

The production infrastructure supporting this roadmap is already in place. The Golden, CO facility is operational. The core engineering team reflects flight heritage spanning SpaceX, Blue Origin, Relativity, True Anomaly, and NASA. The Preliminary Design Review for the LEO assembly demonstration is complete. And the exclusive MIT license on the foundational TESSERAE patent is executed. This Seed round does not fund infrastructure buildout from scratch; it funds the execution of demonstrations on a platform that is already standing.

Overview

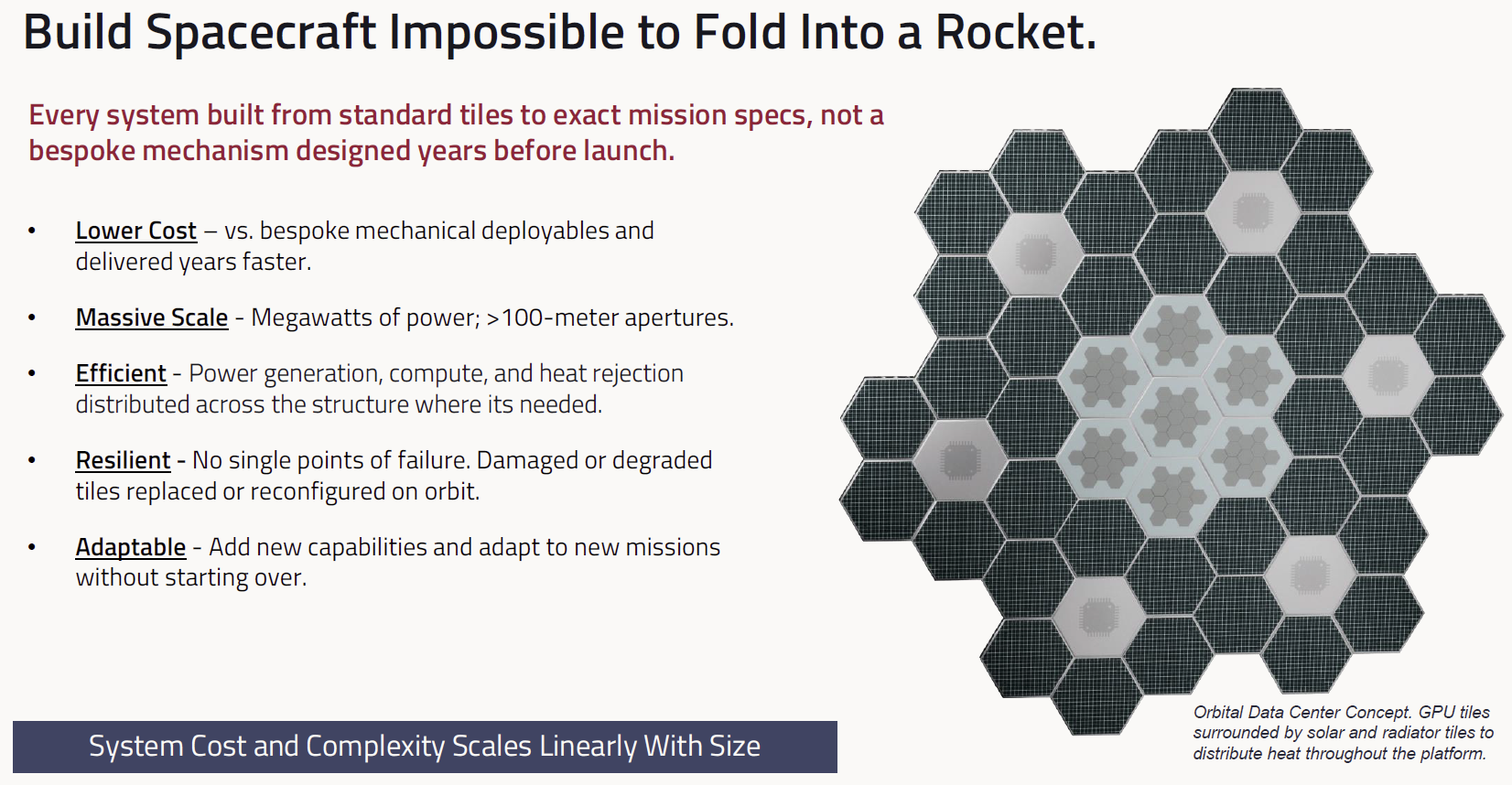

Rendezvous sells tiles: standardized, interchangeable modules that compose into spacecraft of any scale. The company is building a multi-year catalog aligned to the subsystems traditional satellite buses centralize: thermal regulation, sensing, communication, solar power, propulsion, and compute. Every mission expands the catalog, and every new tile type becomes reusable across future missions, strengthening per-tile production economics and the component standard itself. The product is not a satellite; the product is the component system from which satellites are composed.

Three commercial channels are active in parallel.

The Tile: A Hexagonal, Mass-Manufacturable Primitive

The tile itself is the commercial proof point for the entire platform. Each tile is designed for mass-manufacturing at low unit cost rather than bespoke integration, using standard components throughout the autonomy and mesh stacks. Tile-edge interconnects form a dynamic mesh of power and data across the assembled structure, enabling resilient operation: if a tile is damaged, the mesh reconfigures around it or the tile is physically replaced on orbit. This resilience property has no analog in traditional deployable architectures, where a single actuator or hinge failure can render an entire spacecraft inoperable.

For primes and operators, the tile abstracts away the complexity that has historically made large-scale space systems fragile and expensive. A 10-kilowatt, 15-kilowatt, or 100-kilowatt spacecraft is not a ground-up redesign; it is a different count of the same tile. System cost and complexity scale linearly with size rather than exponentially, as they do with legacy architectures. This is the economic property that makes orbital megawatt-class systems viable in the first place, and it’s the property around which Rendezvous is building its long-term moat. Customers are not buying satellites; they are buying capability configured from a catalog, delivered on the rocket of their choice, assembled on orbit.

Strategic Positioning

Rendezvous operates a vertically integrated hardware platform selling tiles and tile-composed subsystems to defense primes, government agencies, and commercial operators. Revenue follows a three-phase path, with each phase pulling forward the next. Phase 1 (Government R&D): SBIR, CRADA, and direct government research contracts at approximately 85% contract margin, funding the technology roadmap while shaping downstream program requirements. Phase 2 (Subsystems): tile-based apertures, power and compute arrays, and space protection shields sold as modular components into prime-built platforms at approximately 75% contract margin. Phase 3 (Full Modular Spacecraft): high-volume tile shipments supplying complete platform integrations at approximately 37% hardware gross margin once the production flywheel reaches scale. Phase 1 shapes the requirements that Phase 2 fulfills; Phase 2 establishes the prime confidence that Phase 3 converts into volume.

The model concentrates Rendezvous on tile production, autonomy, and mission integration while leveraging prime distribution, program management, and regulatory infrastructure already in place. It also generates compounding switching costs: each new mission adds a tile type to the catalog, which makes the next mission cheaper and faster than the last, and every flown tile expands the operational dataset informing the next hardware generation. As facility throughput scales and the tile catalog deepens, the company migrates from project-based integration work into a true component-supplier model with attached software, silicon, and services margin.

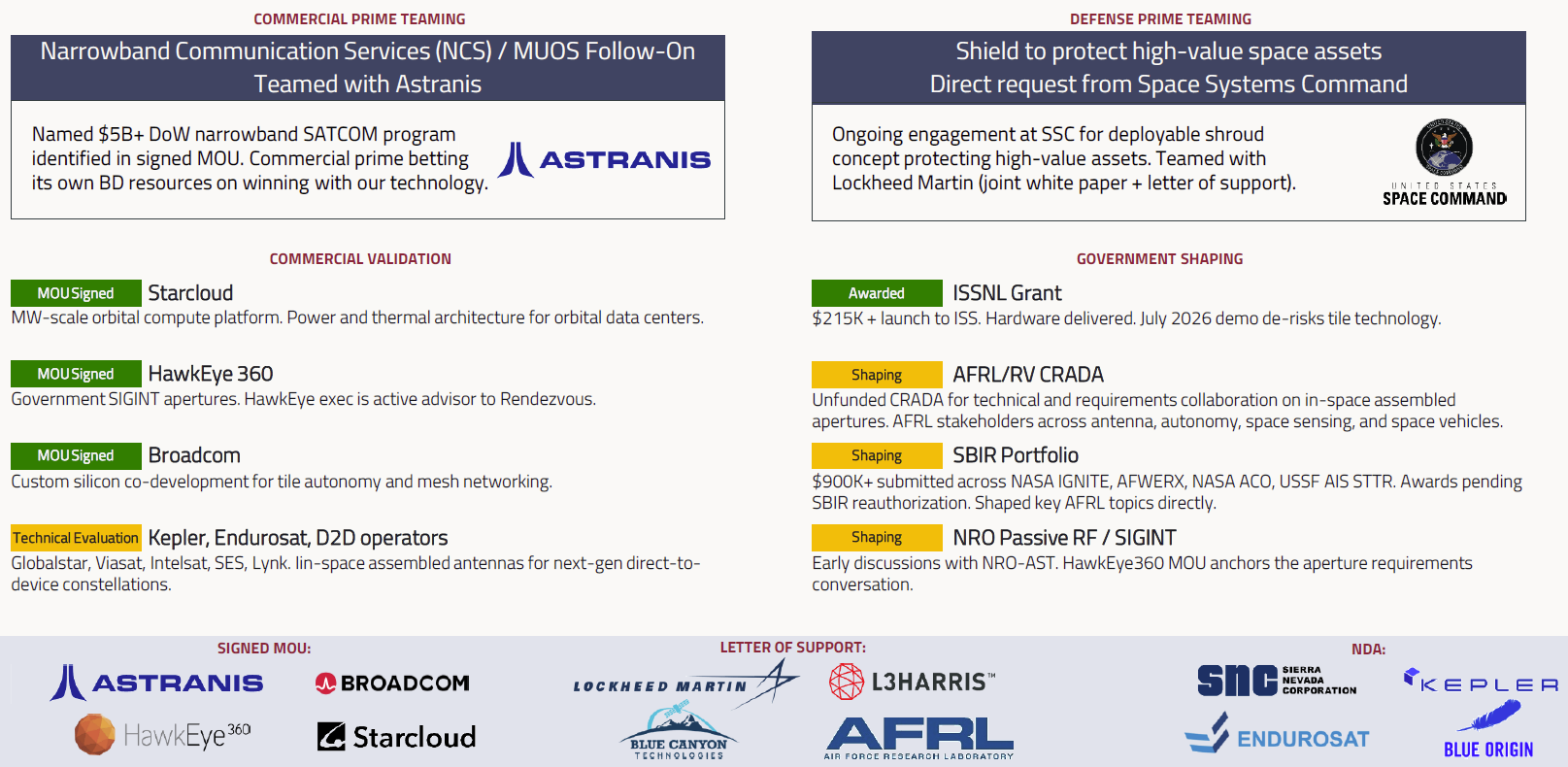

Commercial Validation

Near-term commercial traction is anchored by two strategic workstreams. The first is the Astranis teaming on the $5B+ Narrowband Communication Services program, a named Department of War procurement where the commercial prime has committed its own business-development resources to winning with Rendezvous antenna apertures. This resource commitment is rare at Seed stage and signals unusual confidence in the company's technical readiness and government positioning. The second anchor is Lockheed Martin's SPACECOM-initiated deployable shield concept, supported by a joint white paper and active engagement at Space Systems Command. Together, these pursuits frame the 2026-2028 revenue plan.

Beyond the anchors lies a broad supporting pipeline. Technical evaluations are underway with Globalstar, Viasat, Intelsat, SES, Lynk, Kepler, and Endurosat for in-space assembled antennas. Letters of Support from AFRL, L3Harris, Blue Canyon, and NASA Goddard, plus active NDAs with Sierra Nevada, Kepler, Endurosat, and Blue Origin, demonstrate horizontal demand across the defense prime and commercial operator ecosystem. An unfunded AFRL Space Vehicles Directorate CRADA covers antenna, autonomy, space sensing, and space vehicles — positioning the company to shape requirements that Rendezvous is best-positioned to fill. Over $900K in SBIR submissions (NASA IGNITE, AFWERX, NASA ACO, USSF AIS STTR) await awards pending SBIR reauthorization.

The 2026 revenue plan is intentionally modest ($600K), reflecting the pre-demonstration phase. The inflection is 2027-2028, when a successful LEO assembly demonstration converts the current pipeline into funded Phase 2 contracts and the 2028 RF antenna mission transitions to customer funding. Investors should price this window against partnership conversion velocity, demonstration execution, and prime integration depth.

Partnerships

Partnership quality is the strongest signal in Rendezvous's current posture. The Lockheed Martin relationship — joint SPACECOM white paper plus letter of support — reflects the prime's strategic interest in positioning Rendezvous tiles inside its defense portfolio. Joint white paper programs within Lockheed historically progress to formal teaming agreements and eventual subcontract flow once technical demonstrations land, and Joe Landon's prior tenure as VP of Advanced Programs at Lockheed Martin Space provides direct access to the decision-making apparatus that converts early technical work into programs of record.

The Astranis MOU is structurally unusual. The prime has identified a named $5B+ program (NCS / MUOS follow-on) and is investing its own BD resources to win it using Rendezvous technology — a resource commitment that is rare at Seed stage and signals the commercial prime's confidence in Rendezvous's technical readiness and government-relations positioning. Astranis itself has a strong DoD SATCOM procurement track record, which further de-risks the conversion path.

The Broadcom custom silicon co-development MOU is strategically consequential beyond its immediate scope. Broadcom's leadership in data-center networking silicon positions it as the natural partner to extend into orbital compute, and the co-development path to radiation-tolerant SoCs, mesh networking ASICs, and on-tile AI acceleration maps directly onto Rendezvous's tiered silicon roadmap. This is not a standard vendor relationship; it is a strategic alignment between a category-defining silicon partner and the emerging physical layer for orbital-scale compute.

Secondary commercial validation includes the Starcloud MOU for megawatt-class orbital compute power and thermal architecture, the HawkEye 360 MOU for government SIGINT apertures (with a HawkEye executive serving as active advisor to Rendezvous), and the foundational MIT patent license secured from the originating research institution. On the government-shaping side, the AFRL/RV CRADA and early NRO-AST discussions — anchored by the HawkEye aperture requirements conversation — position the company ahead of competing approaches in key program development cycles.

The in-space assembly category has consolidated around three fundamentally different approaches: human EVA assembly (the ISS paradigm), robotic arm assembly (the current dominant commercial paradigm), and autonomous electromagnetic self-assembly (Rendezvous's category). Each implies different physics, different cost curves, and different mission envelopes — and the transition between them is architectural, not incremental.

Human assembly is functionally retired for large-scale infrastructure. Crewed EVA is too expensive, too slow, and too dangerous to compose commercial-scale spacecraft, and no meaningful program is being built around it today. Robotic arm assembly — pursued by Maxar's OSAM-1 program, Northrop Grumman's SPIDER / MEP work, and adjacent satellite-servicing efforts at Astroscale and ClearSpace — requires every action to follow a pre-planned sequence under continuous human oversight, and it is structurally bounded by the physical reach of the arm. These approaches are useful for servicing and small-scale integration but cannot compose the kilometer-class, many-thousand-tile structures that active program requirements demand. Autonomous electromagnetic self-assembly is a categorically different capability — tiles find each other, align, latch, and reconfigure without human supervision — and it is the only approach physically capable of the scale that orbital AI compute, Golden Dome missile defense, and kilometer-class ISR require.

Today, no direct competitor has flown autonomous electromagnetic tile assembly. The most relevant competitive set spans deployable-structure incumbents, robotic-assembly pursuits, in-space manufacturing adjacencies, and on-orbit servicing companies. As the scale requirement tightens, structurally constrained approaches are positioned to lose ground.

Beyond structural competitors, the most relevant risk is a well-capitalized prime (Northrop, Maxar, Lockheed) choosing to build its own electromagnetic autonomous assembly capability. The eight-year MIT incumbency, the licensed foundational patent, the five generations of flown hardware, and the production-ready Golden, Colorado facility meaningfully raise that replication cost. Sustained flight demonstration velocity — specifically the cadence of successful in-orbit assembly missions — remains the strongest long-term moat.

Rendezvous is raising a $15M Series Seed financing, following a $5M Pre-Seed closed in late 2025 led by Aurelia Foundry and 8090 Industries with participation from ATX Venture Partners, Mana Ventures, and others.

Use of proceeds is gated to two demonstration milestones and targeted operational investment:

Completion of the Q1 2027 LEO demonstration is the single repricing event for the Series A. Successful flight data converts the current MOU pipeline into funded Phase 2 defense contracts, anchors the 2028 customer-funded RF antenna mission, and positions the next round as a growth financing rather than a continued technology-validation financing. The Seed is sized exactly to carry the company to that event with modest contingency, with no need for bridge capital under base-case execution.

Phil Frank, Co-Founder & CEO: Phil brings executive operator depth unusual for a hardware Seed, with prior leadership at Nokia overseeing $5B+ in M&A, earlier senior roles at AT&T Wireless, and three prior startup exits as an AI founder. He has served as both a public-company CFO and Director, pairing capital-markets fluency with product-build execution. At Rendezvous, Phil leads commercial strategy, capital formation, and the transition from R&D to production — anchoring the company's trajectory from stealth emergence to a flight-heritage posture in under two years.

Joe Landon, Co-Founder & President: Joe is the commercial and government-relations foundation of the company. As VP of Advanced Programs at Lockheed Martin Space, he led R&D and business development for a $2B line of business; he previously served as CEO of Crescent Space, CFO of Planetary Resources, and in early engineering leadership at Boeing's commercial satellites business. Joe's Lockheed tenure is particularly consequential given the current teaming structure with Lockheed on the SPACECOM shield concept — arguably the most commercially decisive résumé in the in-space assembly category, bridging prime relationships with new-space operator discipline.

Ariel Ekblaw, PhD, Co-Founder & Board Chair: Ariel invented the TESSERAE technology during her MIT PhD, founded the MIT Space Exploration Initiative, and founded the Aurelia Institute — where the technology was incubated before being spun out as Rendezvous under exclusive commercial license. She remains the technical inventor of record, chairs the Board, and anchors the ongoing R&D pipeline that continues to generate continuation IP beyond Gen-5. Her dual role as inventor and board chair materially reduces execution risk around IP continuity and technical direction.

Gerry Hudak, CTO: Gerry brings SpaceX Dragon 1 and Dragon 2 crewed life support, thermal control, and structures engineering experience, plus Blue Origin lead engineer and ispace US lunar lander Program Manager credentials. He leads the flight systems engineering organization and sets the hardware maturity bar against the most demanding crewed spacecraft programs in industry. His presence as CTO reflects a deliberate choice to apply crewed-spacecraft engineering discipline to a commercial modular platform.

Sean Rogers, CFO: Sean brings Citi-trained finance and space-sector operating experience to the company's capital formation and operating discipline. He supports the Seed close, the manufacturing scale-up that follows, and the Series A pathway, with particular focus on facility financing and vertical integration economics as tile production ramps.

Engineering Bench: The core engineering team reflects exceptional flight heritage density for a Seed-stage hardware company. Brandon Pearce (SpaceX employee #160; acting VP of Avionics across Dragon and Falcon programs) leads Avionics. Luiz Toledo designed Starlink lasercom terminal controls and leads GNC and autonomy. Trevor Sharon built True Anomaly's production floor and manufacturing processes and leads Manufacturing & Test. Alex Miller spent 11 years at NASA designing mechanisms and structures for JWST, Mars Sample Return, and the Nancy Grace Roman Space Telescope, and leads Mechanical Systems. Kyle Lastine built ground and flight software for Relativity Space's Terran 1 and Terran R programs and leads Software. Combined SpaceX engineering tenure across the team exceeds 21 years.

DISCLAIMER: This material is provided solely for informational and educational purposes to support independent investment research and evaluation. It does not constitute, and should not be construed as, investment advice, a recommendation, an offer to sell, or a solicitation to buy any security or investment product. No fiduciary relationship is created by the provision of this information. Recipients are responsible for conducting their own diligence and for making independent investment decisions in consultation with their legal, tax, financial, and other professional advisors. Any views, projections, or forward-looking statements are subject to change without notice and are inherently uncertain. Information presented may be derived from third-party sources believed to be reliable but has not been independently verified, and no representation or warranty is made as to its accuracy or completeness. Investing involves risk, including potential loss of principal. By accessing this material, you acknowledge that it is for research purposes only and agree not to rely on it as the primary basis for any investment decision.