Phoenix Tailings is a US-based metals refining company disrupting the $350B critical materials market.

** Update **

Following the announcement this past Friday that China would be restricting exports of Rare Earth Metals and products to all countries in what appears to be a retaliation to recent tariffs imposed by the US, the importance of Phoenix Tailings' business and technology has become even more significant. Read more on the recent moves from Reuters here, including a quote from Phoenix Tailings Co-Founder & CEO, Nick Myers.

Introduction

Phoenix Tailings is a US-based Series B-stage metals refining company disrupting the $350B critical materials market. Phoenix has developed a novel and proprietary refining process which enables a profitable zero-emission domestic refining operation to meet the needs of the global energy transition. Phoenix is raising a $40M Series B round led by Envisioning Partners with participation from leading investors in the hardtech and cleantech sectors, including In-Q-Tel, BMW I-Ventures, Yamaha, and MPower. The use of proceeds from the round will be to finance the expansion of production from the Company’s current 40 ton per annum (tpa) capacity to a 193tpa capacity to meet the volumes of a $197M supply agreement that the company has signed with a leading rare earth magnet manufacturer.

The global transition from hydrocarbons to critical metals signifies a major paradigm shift in the energy and manufacturing sectors. As the world seeks to combat climate change and reduce greenhouse gas emissions, the demand for fossil fuels is being replaced by the need for critical metals like lithium, cobalt, nickel, and rare earth elements. These metals are essential for renewable energy technologies, electric vehicles, advanced electronics, computing, and even the AI data centers powering the next generation of technological innovation.

See the video below for a look into Phoenix Tailing’s patented and zero-emission critical minerals refining process and how it unlocks a fully domestic supply.

* Significant Current Customer Traction: Phoenix Tailings has secured significant customer traction, with a signed $197M supply agreement with SGI, a leading rare earth magnet manufacturer in the automotive space, and a pipeline of $1B+ from customers in the electronics, industrials, and medical devices space. This existing agreement fully books out the Company's production capacity for 2025 as they expand their modular facility to commercial capacity.

* Proven Technology: Phoenix has fundamentally re-engineered the metals refining process through a proprietary ‘Predictive Complexation’ technology augmented by AI-powered novel chemistry. The Company has discovered a proprietary formulation for rare earth stabilized ion reduction (SIR) salts that can be tuned to enable faster and more efficient reactions, creating a scalable and profitable model for metal refining.

* Geopolitical Climate Tailwinds: At present, Phoenix Tailings has the only operational rare earth metal refinery in the Western Hemisphere and the first end-to-end sustainable process in the world. Existing Rare Earths Metal production is 90%+ based in China & Myanmar with significant environmental repercussions. The US Government has identified rare earth metals as a critical national security concern given its importance in key technologies, with support across all levels of government including the DoD and the Department of Commerce.

* Clean Technology For the Future: Compared to traditional technologies, Phoenix Tailings’ chemistries are designed to drastically reduce the overall process’s environmental footprint. The systems are designed to have zero CO2, chlorine, sulfur, nitrate, or fluorine emissions. While each step in the process does produce CO2, the overall system has zero emissions, creating a sustainable source of critical metals for American and global industries.

* Strong Strategic Investor Group: Phoenix Tailings has built a strong diversified strategic investor group, including notable venture firm In-Q-Tel and strategic investors including Presidio Ventures (Sumitomo Corporation), BMW I-Ventures, and Yamaha. Phoenix Tailings has raised $28M in equity financing to date, in addition to $5M in non-dilutive grant funding from DOE, NSF, Mass Ventures and others.

* Global Market Opportunity: The global critical metals market was valued at $320B in 2022 . This market is composed of various segments, including mining, processing, and end-use applications such as electric vehicles (EVs), renewable energy technologies, and electronics. Due to the relatively high price point and key technology gaps in traditional processing, Phoenix Tailings has entered the rare earth market first before expanding into other critical metals markets

* Strong and Experienced Leadership: Phoenix Tailings' leadership team brings a wealth of experience across strategy, finance, technology, operations, and partnerships. CEO Nick Myers has a strong background in finance and partnerships, with leadership roles at Meenta and SparkCharge, and a foundation in physics and business. Co-Founder and Advisor Michelle Chao brings operations and engineering expertise, including successful product launches and R&D leadership in 3D metal printing. CTO Dr. Thomas Villalon Jr. is a distinguished technology expert with a PhD in Materials Science & Engineering, specializing in novel materials processing. VP of Partnerships Anthony Balladon has a diverse background in commercial strategy, research, process engineering, and private equity analysis.

Plum Alley Ventures Company is presenting this Series B investment as a new opportunity in Phoenix Tailings. This round is led by Envisioning Partners Impact Fund ($140M+ in AUM), with participation from In-Q-Tel and strategic investors including Presidio Ventures (Sumitomo Corporation), BMW I-Ventures, and Yamaha. The Company initially set out to raise up to $40M at a $130M pre-money valuation, but due to investor interest the round was extended to be up to $60M, with $41.3M currently funded.

The primary use of proceeds will be for the Company's next refining facility and its first fully integrated commercial-scale refinery, capable of fulfilling the $197M contracted offtake agreement. This facility represents the primary capital buildout from the Series B raise, with $13M allocated for CAPEX, and is expected to generate $20M in annual revenue at full production, and $5M in gross profit.

More information on the terms of the round can be found in the ‘Capitalization & Current Raise’ Section below.

INVESTMENT TIMELINE

Virtual Founder Discussion

Tuesday, Tuesday, January 20th, 2026,

12:00pm ET // 9:00am PT

RSVP to Google Calendar Invite

Zoom Call Details Available Here

Final Investment Commitments Due

Monday January 26th, 2026

We will take commitments on a rolling basis. Please submit final commitments here.

Funding & Documents Due

Monday January 26th, 2026

At the end of the commitment period, you will receive details regarding closing documentation and wiring instructions via Carta.

The Company's confidential financing documents and diligence materials are available for review in DropBox. Please request access to data room materials at the top of the page. All documents are confidential and not for further distribution. If you have specific questions or are interested in investing in Phoenix Tailings, please contact us and submit your investment total here. Given the expedited Syndication timeline to meet Phoenix's Series B closing date, if the PAVC Syndicate does not meet certain milestones it may not move forward.

Global Need for Critical Metals:

Phoenix Tailings is built to be the world’s first fully clean mining and metals production company, creating the needed materials for the energy transition and the advancement of high-end technologies. Phoenix’s long-term vision is to build a fully vertically integrated business to produce rare earth metals (REMs) and other critical metals from non-traditional sources such as Tailings. Rare earth metals have become essential components in the rapidly evolving landscape of climate technologies and computing, and remain critical components to traditional electronics, automotive and medical device manufacturing given their unique traits and capabilities. These materials sit at the intersection of two major technological trends: the transition to clean energy and the explosive growth of AI computing infrastructure. However, global supply is dominated by China and Russia, which control 95%+ of refining operations, in part due to the significant environmental impact existing processes have on surrounding areas.

What are Rare Earth Metals:

Rare earth metals were first discovered in Sweden in 1787. Throughout the 19th and early 20th centuries, scientists gradually isolated individual rare earth elements, but their commercial applications remained limited due to the complexity of their extraction and separation.

Rare earth metals, despite their name, are relatively abundant in the Earth’s crust, but they are significantly less common than metals like iron and copper. However, unlike iron and copper, which occur in high concentrations and easily minable ores, rare earth metals are typically dispersed in low concentrations across a variety of minerals, making their extraction and separation far more complex and resource-intensive.

It wasn’t until the mid-20th century that their unique properties, particularly their exceptional magnetic, luminescent, and conductive characteristics, were recognized as essential for advanced technologies. The development of powerful neodymium-iron-boron (NdFeB) magnets in the 1980s revolutionized industries such as electronics, clean energy, and telecommunications, cementing the importance of rare earth metals in modern manufacturing.

Rare Earth Metals Use Cases:

The fundamental characteristics of rare earth metals, including their high magnetic strength, heat resistance, and conductivity, make them indispensable in applications that require miniaturization and high efficiency.

For instance, neodymium and dysprosium are used to create powerful permanent magnets that improve the performance of EV motors and wind turbines by enhancing energy conversion and reducing power loss. Lanthanum and cerium are critical in battery technology and catalytic converters, while yttrium and europium are key components in advanced medical imaging devices and LED displays. In data centers and high-performance computing, rare earth elements contribute to the efficiency of cooling systems and the development of high-speed processors.

Their unmatched ability to maintain stability at high temperatures and their superior magnetic and conductive properties make rare earth metals irreplaceable in modern technologies, driving innovation across industries.

Supply Chain Challenges:

Manufacturers dependent on rare earth metals (REMs) face significant supply chain challenges across mining, refining, and production stages. These challenges include:

This concentration creates significant vulnerabilities for manufacturers, as evidenced by China's past export restrictions to countries like Japan in 2010-2011 1. The monopolistic control allows China to influence global prices and availability of these critical materials.

These issues underscore the need for sustainable, reliable and domestically sourced and produced rare earth metals to maintain and expand critical supply chains for these industries.

Predictive Complexation

Phoenix Tailings is on a mission to become the world’s first vertically integrated manufacturer of rare earth metals. To accomplish this, the company completely redesigned its chemistry and reaction kinetics to enable scalable and repeatable refining methods. The fundamental breakthrough that Phoenix discovered is a proprietary formulation for rare earth stabilized ion reduction (SIR) salts that can be tuned to enable faster and more efficient reactions – this is the basis of the company’s “Predictive Complexation” approach, which leverages a series of proprietary algorithms and models to create novel chemistries for each step of the extraction and refining processes.

Specifically for refining, Phoenix’s trade secret methods force the metal ions to form novel complexes in a chemistry known as coordination chemistry, where metal ions (lewis acids) form bonds with cation ligands (lewis bases) in ways that stabilize the molecules in the molten state. By creating certain desired metal-ion complexes, the process of refining metals can be greatly enhanced – so much so that the company can completely redesign the equipment to process the refining to enable continuous, closed-off, more energy efficient, and zero waste production systems with very long cell and electrolyte lifetimes.

The breakthrough chemistry, which is also highly scalable compared to traditional chemistries, enables the entire system to work cheaper, faster, longer, and with less emissions. All of these improvements have led to a significant (and growing) patent and trade secret portfolio.

Overall, Predictive Complexation drives not only chemistry improvements, but also equipment and process improvements that when combined enables a truly disruptive end-to-end clean metal production platform.

Refining: Separation & Metallization

As discussed above, the process of refining metal is broken down into two core components: separation, and metallization.

To date, Phoenix Tailings has produced the metal below at their Burlington MA pilot production facility:

The company has also run separation circuits for over 1000 hours, producing NdPrO3 from market carbonate concentrate, further converted to 99.9% NdPr metal.

Phoenix Tailings currently purchases concentrates from traditional sellers, but in the future will be able to extract its own concentrate directly from tailings sites. The company’s extraction technology will bring a paradigm shift to the mining industry – rather than continuing to destroy the planet to access new ore bodies, Phoenix is building a future in which the company cleans up the planet by harvesting what are currently considered valueless toxic tailings that actually have exponentially more resource availability than traditional sources.

Intellectual Property

Phoenix Tailings has filed 18 families of patents in the US and internationally. 4 patents have been issued in the US, with 15 pending non-provisional patent applications and 7 pending provisional patent applications. Phoenix Tailings’ overall IP strategy can be broken down into two core categories with novel chemistry formulations developed by its Predictive Complexation technology protected with trade secrets and the enabling hardware and processes for commercialization protected by patents.

Phoenix Tailings’ business model is to source concentrates as an input, extract, and refine the metals within them, and sell final metal products (initially rare earth metals but will expand into other critical metals) to customers. Initially, Phoenix is currently purchasing concentrates from various suppliers on the market. However, in the future, the company will source its own concentrates by securing tailings sites – this will help drive dramatic margin expansion.

The direct sourcing of concentrate from tailings brings in an additional opportunity for value creation. Phoenix’s strengths in minerals exploration and development helps the company acquire legacy tailings sites at low costs, which will then be economically characterized and de-risked in order to either obtain low-cost financing or be sold at a premium, generating substantial return compared to the capital required to develop them.

Key Markets

OEMs and End Manufacturers: End OEMs and Tier-1 suppliers are the major end customers for Phoenix Tailings. They are the ones driving the push to a Non-China supply chain down to their suppliers. It is often they who make the final decisions on rare earth deals, even when the actual contract is with a magnet manufacturer.

Magnet Manufacturers: Magnet companies are the primary users of Phoenix’s product, converting the metals into magnet form. There are 7 major established manufacturers outside of China, three of which have signed MOUs with Phoenix Tailings. All of these magnet manufacturers have extensive growth plans and are collectively constructing ex-China capacity totaling 25,000 tpa of magnets (requiring ~9,000 tpa of metal) by 2028. Given that US demand for ex-China magnets is projected to reach 10,000 tpa by 2030 with Europe and Asia reaching approximately 50,000+ tpa, a growing incentive for new magnet manufacturers to enter the market is expanding the overall size of this market.

Commercial Traction

To date, Phoenix Tailings has secured commercially contracted metal sales of $197M through 2031 with SGI in Korea, one of the world's largest magnet manufacturers. In addition, Phoenix has an increasingly robust pipeline of signed non-binding MOUs worth over $1B.

Secured Offtakes

MOUs & Pipeline

Beyond the initial traction, Phoenix has built a robust pipeline of over 430 active deals across the entire spectrum of industries. In the context of this pipeline, MOUs are considered in the “Negotiating” stage. Further details on the Company’s financial projections can be found in the Data Room.

The global critical metals market was valued at $320B in 2022. This market is composed of various segments, including mining, processing, and end-use applications such as electric vehicles (EVs), renewable energy technologies, and electronics.

Notably, a report from the DOE at Argonne National Labs estimates the demand for rare earth magnets growing nearly 600% by 2050. This puts tremendous pressure for manufacturers to diversify supply chains and lock up long term supply agreements.

Key Segments

Due to the relatively high price point and key technology gaps in traditional processing, Phoenix Tailings has entered the rare earth market first before expanding into other critical metals markets. Phoenix Tailings currently focuses on three rare earth pure metals and two metal alloys which are outlined below that are used to make magnets. Prices for calculation are taken from Shanghai Metals Market.

The markets can be volatile, with the price per kilogram (kg) of DyFe, NdPr, and Tb fluctuating dynamically. However, since Phoenix will be buying market oxides initially until separation is online, and those oxide prices tend to mirror the final metals price, margins are insulated from volatility in the short to medium term.

Phoenix aims to be the first domestic fully vertically integrated rare earth producer. Across each part of the value chain, Phoenix also has key competitive advantages over both existing traditional rare earth refining techniques as well as from emerging players in the industry.

Separation

In separation, Phoenix’s is mainly competing against existing separation facilities used in traditional rare earth refining. However, there are several companies in the US that are working to scale up their separation capabilities – these include Energy Fuels, General Atomics, MP Materials, and potentially USA Rare Earths.

While the equipment for separation is off-the-shelf, Phoenix has significant technical advantages. Phoenix has redesigned the flow sheets to require less equipment, 80% less labor, 65% less reagents and 60% less energy. As a result, there is an overall 38% OPEX improvement over the traditional separation process. This is due to the company’s predictive complexation approach to design novel chemistries.

Metallization

Phoenix’ aims to be the only domestic fully vertically integrated rare earth producer is primarily made possible by its proprietary metallization capabilities. While other companies may be able to mine or separate rare earths, being able to metalize the oxides persists as highly difficult for others to replicate outside of China. One exception is Less Common Metals, a UK-based company that has attempted to introduce the Chinese metallization process outside of the country. However, they have very limited production capacity and have not achieved significant market traction, likely due to unfavorable unit economics facing the Chinese-metallization process.

Further details on the Company’s competitive advantage can be found in the Data Room.

Capitalization

Prior to the current Series B round, Phoenix Tailings has raised a total of $28M across Series Seed ($1.68M, 2020), Series A ($8.8M, 2021), and Pre-Series B SAFE ($17.5M, 2023) rounds. Additionally, the company has received a total of $4.9M in non-dilutive government funding from the DOE, NSF, Mass Ventures and others. Most recently, this includes the $1M ARPA-E ROSIE grant, demonstrating third party validation of the company’s innovative iron technology.

Notable investors in Phoenix Tailings include:

Phoenix Tailings has secured a diverse group of investors that have the capability to support the Company both in future financing rounds and in industry connections and support.

Series B Use of Proceeds

Today, Phoenix Tailings has scaled its refining technology from lab to pilot scale in its Burlington, MA facility, and is producing products to satisfy its commercial offtakes. The proceeds from the Series B will go towards scaling the refining operations up to a profitable commercial scale facility, which will enable the company to deliver on its first major commercial contract and unlock future commercial facilities which will be funded by project financing.

Series B Financing Terms:

Nick Myers (Co-Founder & CEO)

Strategy and finance leader. Prior to Phoenix, Nick was Director of Finance and Partnerships at Meenta, COO at SparkCharge, and Lead Associate at Techstars Boston. Nick also Founded and was a Director at Northeastern Angels. MBA from Northeastern University and a B.S. in Physics from Saint Michael’s College.

Michelle Chao (Co-Founder & Advisor)

Operations and engineering leader. Prior to Phoenix, Michelle was a Technical Product Manager at Markforged, where she managed the materials product portfolio, launching five new material products in 2019 alone. Her leadership in a project that doubled print speed was instrumental in helping Markforged achieve a $25M quarterly revenue milestone. As a Materials Engineer, Michelle led R&D efforts for a novel metal 3D printing platform, overseeing the design and management of a metallurgical analytical lab.

Dr. Tomás Villalón Jr. (Co-Founder & CTO)

Distinguished technology expert. Prior to Phoenix, Tomás was a Research Scientist at Digital Alloys, where he developed analytics and computational models to optimize the Joule Printing Process. Ph.D. in Materials Science & Engineering from Boston University, pioneering solid oxide membrane processes for high-purity silicon and aluminum production. B.S. Materials Science & Engineering, MIT.

Anthony Balladon (Co-Founder & VP, Partnerships)

Commercial and strategy leader. Prior to Phoenix, Anthony was a Research Analyst at Mintek working on hydrogen fuel cell technology development, Process Engineer at Colibri leading feasibility studies and client relationship management, Private Equity Analyst at a Search Fund Accelerator, and Business Development Consultant at Crimson Hexagon. Bachelor in Chemical Engineering from the University of Cape Town and Master of Science and International Business and Finance from Hult International Business School.

Rick Salvucci (VP, Downstream Processing)

10 years of experience in optimizing and scaling electrochemical processes. Led scale-up efforts at Infinium, Inc. for Nd, NdPr, DyFe and Al-Master alloys as Development Engineer & Project Manager. Currently leads metallization and separation engineering development at Phoenix Tailings.

Alex Nyarko (VP, Upstream Processing)

Over 20 years of experience designing and commissioning new mining and metals production facilities. He began his career as a Metallurgist involved in the day-to-day operation of a gold processing plant owned by AngloGold Ashanti. He then went on to join the EPMC & design houses, working in numerous geographical areas and locations.

Disclaimer

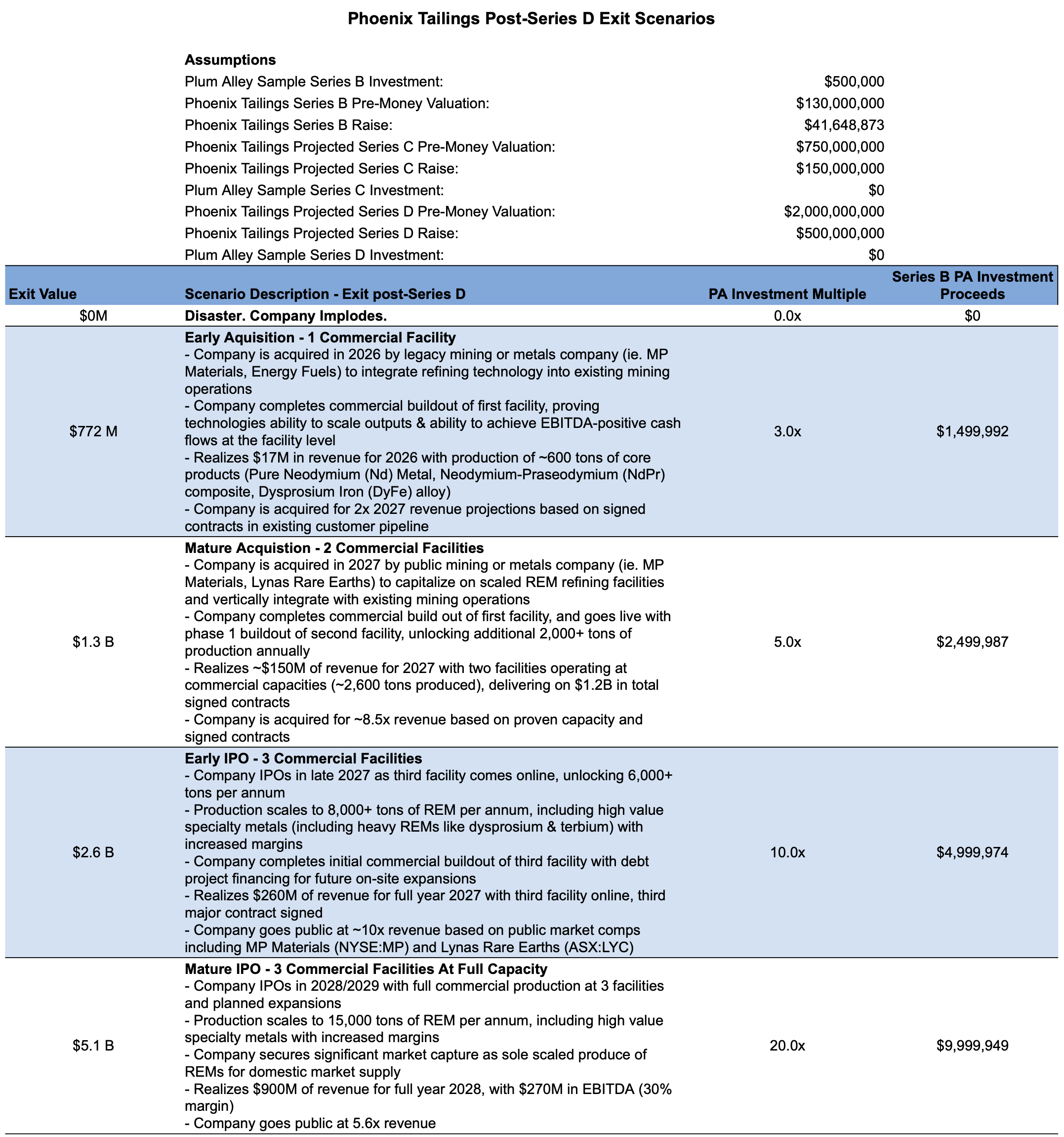

The following information is presented for illustrative purposes only and contains numerous assumptions that may or may not occur. Investors should perform their own assessment, and are cautioned that milestones mentioned below may or may not be achieved, and that other milestones and/or material events not named here could occur to alter the valuation and outcome. Investors should make their own assessment and determination on valuation and potential return, with the information below only as a guide. A full summary of several potential scenarios has been provided in the appendix.

Exit Analysis Assumptions:

PAVC analyzed some theoretical exit scenarios with support of some key assumptions. The exit analysis below assumes:

The assumptions used to support the scale of each exit included:

Phoenix Tailings provides an opportunity to capitalize on the macro-environmental trend of increased usage of rare earth metals (REMs), as they are essential components for technology-enabled societies today. Demand for REMs from governments, businesses, and consumers alike has steadily grown as more advanced technologies continue to expand across industries. This surge in demand is driven by the widespread adoption of electric vehicles, renewable energy infrastructure, and cutting-edge electronics, alongside national initiatives focused on reducing dependency on foreign supply chains. As technological innovations such as artificial intelligence, quantum computing, and 5G networks proliferate, the reliance on REMs is set to increase even further. Phoenix Tailings stands at the forefront of this trend, offering a unique investment opportunity to tap into the growing need for sustainable, domestic sources of these critical materials, while also addressing the pressing challenge of environmental responsibility in the extraction process.

Considerations with this opportunity include both market and business associated risks, which are: